- cross-posted to:

- [email protected]

- cross-posted to:

- [email protected]

The article itself is Dutch, so below is an English translation:

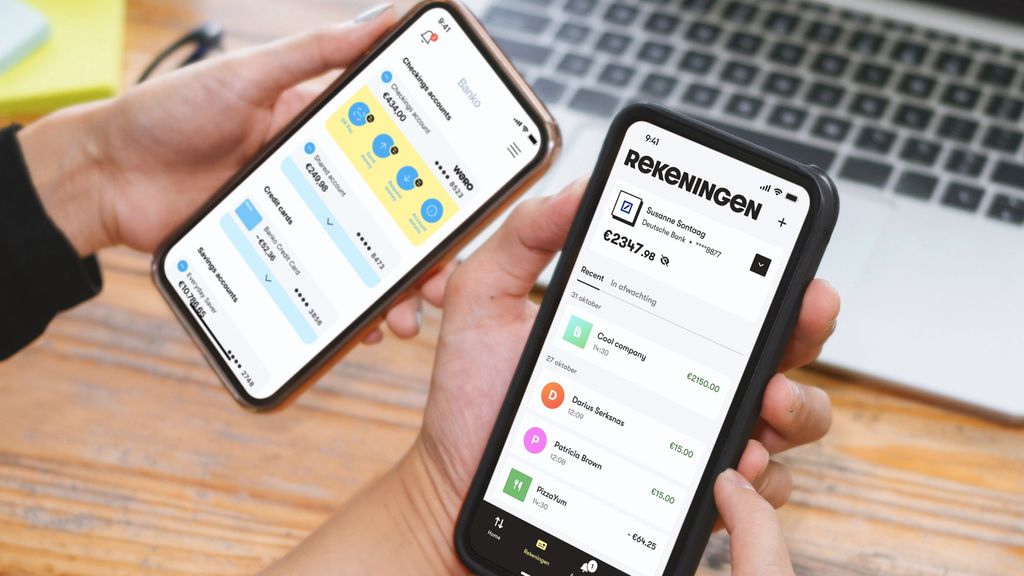

After twenty years, the popular payment method iDeal will disappear step by step over the next year. The name of the method to make online payments and transfer money changes to Wero. That is the European variant of iDeal which was conceived by Dutch banks.

For anyone who pays with iDeal now, nothing is changing, emphasizes Amos Kater of iDeal’s owner Currence. So don’t fall for scams, he warns: “There will probably be fake emails and messages in which scammers say you have to change your data for Wero. Don’t do that, because you just keep paying with the bank’s app, just like you do with iDeal.”

The Dutch banks launched iDeal in 2005. Until then, buying online was coming off the ground slowly because each bank had developed its own methods for paying for something online. With iDeal, stores had to offer only one payment method on their website.

The Dutch success led to the creation of a new company a year and a half ago, in which the Dutch banks together with those from Belgium, France, Germany and Luxembourg made a European variant of iDeal. Because the name iDeal did not have an equally fortunate association in every country, a new name was chosen: Wero, a merger of ‘We Euro’.

Now that banks in Germany, Belgium and France have rolled out Wero over the past year, the familiar name iDeal will slowly change to Wero in the Netherlands in the coming year. “On webshops you will see a new logo with iDeal/Wero from January. It’s not more than that,” Kater explains the change. “With this new logo, we want to make it clear that iDeal and Wero belong together. And that you can also have the confidence of iDeal in Wero.”

Later in the year, it is tested step by step whether the Wero system works error-free with online payments. At the end of next year, the first webshops will switch to the technical system of Wero. Kater: “In 2027, iDeal will be phased out completely.”

With Wero, webshops get a large group of extra customers. With iDeal, only Dutch consumers can pay. With Wero, Belgian, German and French customers will also be added with the same payment method. Luxemburg will follow soon and there will also be discussions with Austrian banks. “The ambition is every country in Europe,” says Kater.

Consumers who want to buy something elsewhere in Europe do not need to use a credit card, PayPal or other payment method. And not only on the internet, Kater says: “For example, if you want to charge your electric car abroad, you can also pay with Wero via your own bank app.”

In addition, iDeal will be expanded with some new features. The most important thing is a purchase protection: “If a product is not delivered, your rights must currently be honoured by the webshop. With Wero, this will soon be done through your bank, just like you can with a purchase via a credit card. Or you can set the money to be debited from your account only when the product is delivered.”

It will also be possible to pay for subscriptions automatically via Wero, as an alternative to direct debit. “That function can also be very interesting for shops, associations and charities,” Kater believes.

The Consumentenbond (Consumers Union) calls the transition from iDeal to Wero “promising,” especially as it can be a good substitute for payment services from large U.S. companies.

In Europe, virtually every country has its own systems for identification and online payment. American competitors such as Mastercard, Visa, PayPal and Apple Pay give Europeans the opportunity to pay with the same method everywhere.

Europe fears that the disabling of the systems of, for example, Mastercard and Visa can be used to put political pressure on the continent. European banks believe that Wero should become the European alternative to this.

Glad to see we are finally making the jump! Also glad that people are seeing the threat of relying on American payment services, and that potential that Wero has to help deal with that threat.

You must log in or register to comment.

Go Netherlands! Finally some good steps towards an EU payment provider.

I’d still prefer GNU Taler, but this is nice too.

I mean we’ve had ideal for twenty years, about time the rest of Europe caught up!

Wero is going to be better than iDeal. One of the biggest downsides of iDeal for consumers is that the moment you hit the pay button your money is gone from your account and there’s no easy way to get it back, even if the webshop never gave you what you paid for. This meant that it was safer to use credit cards for most online purchases, unless you knew and trusted the webshop. Wero is supposed to have similar consumer protection to credit cards, so it should be much safer to use on random-ish webshops that aren’t big brand names. I can’t wait until everyone supports it!

The safety is a plus, but credit card protection is a downside for sellers (disputes are expensive). Additionally, Wero fees are going to be higher than iDEALs fees (percentage-based rather than fixed fee) which will cause some inflation.

It’s a nice step forwards but not one without downsides.

Didn’t know about the fees, that is indeed a shame. Probably needed to provide meaningful consumer protection though. And I don’t really care that providing that protection is a downside for sellers, for them it’s just part of doing business, for consumers it can be quite catastrophic when they’re swindled.

Nice, this would be nice to have.

But also, fuck you Netherlands: I’ve been there a couple times and there was quite a vast amount of shops who did not accept cash, only card payment. This is unacceptable: Euro is official money, not whatever number is in your bank account.

The most German thing I’ve read this morning.

I’m not German.

You don’t have to be German to say something profoundly German 😛 Germans are famous for not accepting electronic payment.

I am Italian, I’m not talking about shops not accepting card payments: that is completely fine and should be an option in all shops.

What I’m saying is that it is unacceptable for a shop in the Eurozone not to accept Euro as payment.

They can not do that because it is illegal and because it devalues the value of Euro. I’m fine paying with the card, but I’m not taking my card out to pay 1€.

When I first saw it I decided not to pay unless they gave me the option to pay with cash, in the end I had to pay with the card as I could see the shopkeepers freaking out.

The creditor of a payment obligation cannot refuse euro banknotes and coins unless the parties have agreed on other means of payment.

https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32010H0191&qid=1604311928631

Europe fears that the disabling of the systems of, for example, Mastercard and Visa can be used to put political pressure on the continent. European banks believe that Wero should become the European alternative to this.

If google and apple remove the european banking apps from their stores, there is no official channel to get to wero anymore. The google play store and apple app store most likely has the ability to uninstall apps without user interaction too.

People who don’t like this dependency in the first place will not be using wero anyway.

Am I just living in a different reality to everyone else?

That’s a whole other level of dependency. The dependency on Google/apple also sucks, but it’s still better to be only dependent on Google instead of Google and MasterCard.

They could have mandated to integrate Wero into Onlinebanking web interfaces, right next to instant SEPA transactions. They could have made Wero an open API like extending the 20+ year old HBCI/FinTS standards. Lock in to proprietary apps exclusively distributed in google’s and apple’s store is a conscious choice and not one I need to find “better” than anything else.

GNU Taler shows how you can do it right, but of course for really open systems there is no big ad campaign money.

Well, who is “they”?

Wero is a private european company (SE) owned by private banks. They made these choices consciously, and even then it’s not uniform: some banks integrate Wero into their online banking apps, some banks use the standalone app instead.

Wero is not a EU project, it’s merely “supported” by the Commission and the ECB.

they = EPI in this case, but we can also dream that the European Union as a whole could mandate that “critical infrastructure” (to be defined) must be available outside of american app stores.

Don’t let perfect be the enemy of good. The EU is not aiming for digital independance, it is merely targeting a critical dependency.

The play store/services are not a critical dependency. If Google cut Europe out, it would be worked around in days or weeks, even if by side-loading, which severely limits Google’s usefulness as a potential economic weapon. However no amount of side-loading can fix non-sovereign payment infrastructure disappearing, hence the urgent need for sovereignty.

Don’t let perfect be the enemy of good.

I saw people say this a couple of times and still don’t quite know what that means.

I mean I will respect EPI’s wishes for only Android and iOS users to use Wero, and not use it, but can’t say I understand what “Don’t let perfect be the enemy of good.” in this context is supposed to tell me.

That depends entirely on how Wero works (with which I have no experience yet because I do not have access to Wero until my bank rolls it out next year) for in-store payments

If Wero works by simply scanning a QR code, and not through NFC (Apple or Google Pay), there is no dependency. It’s just data being transferred through a visual code, with which you can independently communicate with your bank’s servers.

That is how it used to work with iDeal for online purchases anyway… So I don’t see why you cannot use the same method for in-store payments.

Edit: I think I misunderstood what you were referring to. You are referring to the apps being installed on phones running Android or iOS. Not using Google Pay or Apple Pay to verify the payments.

That is a different problem that probably needs to be tackled separately. There are de-Googled versions of Android that could hypothetically gain traction, but even if that happens it would take years for people to swap out their phones as they become old.

Sideloading is also a way in which you could hypothetically get existing phones back up and running after apps get removed (for Android anyway, not so much for iOS)

Sideload from where? Aurora Store works by using a pool of real Google Accounts that google may ban at any time. Third party websites that host android apps typically won’t have a license to redistribute proprietary apps, but they also are somewhat tolerated I guess. On top of that the typical end user will have a hard time verifying that apps from third party hosting sites will not be tampered with and re-signed with a different key.

With banking apps it’s also like 50:50 if they work on an AOSP phone without google play services, or on aliendalvik on SailfishOS or on waydroid on Ubuntu Touch and other open smartphone OS. Personally on my Ubuntu Touch phone I don’t bother with waydroid, running a stripped down android in a container doesn’t seem like a good model to me. If Europe actually wants to “standardize” on Android Apps, we should first have a portable android runtime with a well defined set of APIs that apps are restricted to using in order to be portable.

Sideloading is simply a matter of installing an APK file onto your phone. Where that APK file comes from does not matter.

If Google bans the banking apps I cannot imagine that the banks will just accept and tolerate that without a fight. They would be the ones likely distributing their own app

“Go to Rabobank.nl, and download our Rabobank app”

and why don’t they do that now?

Because people expect their app to be on the app store, and the app store is still available?

Sideloading is more of a pain for the average user compared to just downloading it from the app store, and as long as it isn’t necessary there is not much reason for banks to accomodate it. However, that doesn’t mean that once it becomes a necessity, it’s impossible to set up methods involving sideloading to get around restrictions from Google.

Edit: As an example, the Chinese have Android phones, but the Google Play Store is not available in China. They have different app stores to “sideload” applications onto their phones. In theory they could also install APKs, if that is how apps would be provided to them.

Feel free to ignore my rants btw, I know they are inconsequential. It’s just that you can only read so many threads about mobile operating systems that aren’t US controlled where someone immediately goes “But will my banking app work on this?” “I can’t use this if my banking app doesn’t work on it” “I need my banking app to work to use this” “banking app” “banking app” “banking app”. Personally I’ve never used one of those banking apps and don’t plan to, as long as they are platform locked and have no open documented interfaces, but they are obviously just one of the many pieces of software that prevent people from using something other than an US controlled mobile OS.

I don’t quite remember if it was https://archive.fosdem.org/2023/schedule/event/eu_app_stores/ but it have been. I had still “pirated” my public transport app from the google play store for an android phone without play services at this time and briefly talked with the speaker about it. I think that was the time that really convinced me to just not support any exclusive apps anymore. I mean in the end it doesn’t matter if it was that specific talk or not, because the issues stay the same, only the years change.

In 2027 :( takes long. Can’t wait to send tikkies to the Germans in my life.