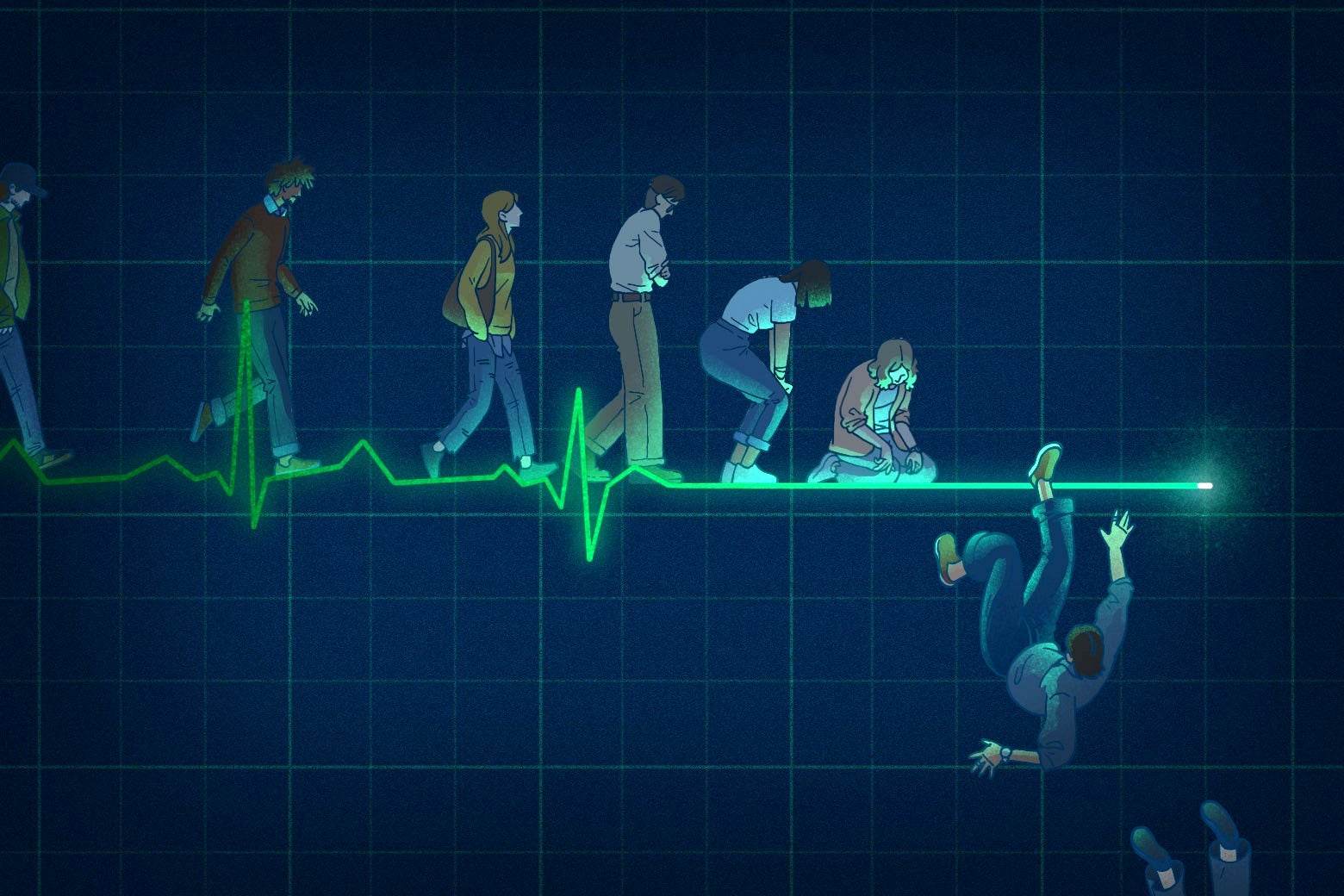

Younger millennial, single, small one bedroom apartment that isn’t fancy, 2 cats, no kids. I didn’t get to go to college after high school, my parents weren’t about to help me, either financially or practically, and I just couldn’t figure out the paperwork/admin nor could I have afforded it myself or gotten loans without a cosigner. I eventually got an ok paying job that required a certification. I work anywhere from 40-70 hours a week and I can still barely afford to pay my bills. I’ve gone over a month without buying food and lived off whatever free food I can grab at work. I’m slowly working my way through a college degree that I’m unenthusiastic about, but I got denied financial aid because I have to make enough to live and cover my rent like an adult and FASFA looks at my annual income and thinks that since I don’t own a house or have kids I have no living expenses and that I can easily afford 30k in tuition every year, so I’ve gotten zero grants or scholarships and at this point I’m only trying to finish my degree so I have something to show besides my stupid loans. I’ve been putting away a portion of my income in a matched 401k for the past 10 years but lot of good that did me, it’s lost far more money than it’s ever gained, and it’s expected to give me a mind blowing $15 a month when I retire if I continue at the current rate.

My retirement plan is suicide, but more and more I don’t see why I’d wait for retirement age. I have no time or money for hobbies and there’s nothing in my life that brings me joy besides my cats. I think once they’re gone I’ll go with them.

How did your 401k lose more than gained. That would basically be fraud. Just doesn’t work that way. And you left out that you are technically disabled (adhd). I’m not saying shit ain’t fucked up, but this story seems an exaggeration.

How did it lose more than it gained? The loss in interest in investment plus the yearly management fee from the company my employer chose to manage the stupid thing is more than the gains during the good years? I’m no investment expert, all I know is that anytime it gains money it then loses all that shortly after. I’d be better off putting the money in a savings account except at least this way I get employer match.

And sure I have ADHD, but it’s not like I’m disabled and unable to work, I’m still working and going to school. You want to tell me that I shouldn’t be able to support myself working over 40 hours a week (and I am not working a minimum wage or “low skilled” job)

If they’ll let you take it and put it in your own 401k I’d suggest doing that. Choose a low-fee brokerage that doesn’t fuck with your investments to incur fees. That’s how they make their money, by taking yours. Choose index funds and let it ride, keep adding when you can, don’t mess with it.

If losses and fees over 10 years came out negative, that is an extremely high indicator of fraud. There are a few exceptions. 1, if you hand picked the investments. 2 if the investments are restricted to like only the company you are working for, which I think has another name instead of 401k.

In the last 10 years the general market is up over 200%.

As for adhd. The point was you are technically not the average person. For us adhders college specifically is often extremely hard. Grades in general before college are rough too, which in turn reduces options for colleges. So it puts us at a solid disadvantage over the average. It certainly is a range, similar to how autism is a spectrum. And adhd can cause some sysmptoms most commonly associated with autism. Some people with adhd can’t work. Those that can often get paid less than thier peers.

In another comment you mentioned that ICE gets a hiring bonus of more than your annual salary. The bonus was $50k I believe. These days for someone in their 30s, that is pretty low for a lot of places except those with a low cost of living.

All in all, you should keep an eye out for that one coworker who seems to know all the details of the 401k and other benefits. Get to know them, and ask questions. They usually love to talk on the subject and can probably help you understand how it all works better. I suspect thier are things you don’t know about that make the situation better than it seems.

I don’t know about the other stuff, but I had a job from late 2021 to early-mid 2023. By the time I left the job, the net contributions over about 18 months were $9,992.78, and the balance was $10,340.83.

From the 2nd through the 11th month, the balance was literally less than net contributions.

18 months is very short for a 401k. They usually say to start looking to move the money out of the volatile market and in to stable investments 5 to 10 years before you need it so that you can avoid short term down markets and maybe catch some high spikes.

I’m with the other commenters, baffled about your 401k comments. I changed jobs in 2017 so the 401k I had with that company is a good case study. It’s doubled its balance without a single contribution (obviously, since I left that company).

Younger millennial, single, small one bedroom apartment that isn’t fancy, 2 cats, no kids. I didn’t get to go to college after high school, my parents weren’t about to help me, either financially or practically, and I just couldn’t figure out the paperwork/admin nor could I have afforded it myself or gotten loans without a cosigner. I eventually got an ok paying job that required a certification. I work anywhere from 40-70 hours a week and I can still barely afford to pay my bills. I’ve gone over a month without buying food and lived off whatever free food I can grab at work. I’m slowly working my way through a college degree that I’m unenthusiastic about, but I got denied financial aid because I have to make enough to live and cover my rent like an adult and FASFA looks at my annual income and thinks that since I don’t own a house or have kids I have no living expenses and that I can easily afford 30k in tuition every year, so I’ve gotten zero grants or scholarships and at this point I’m only trying to finish my degree so I have something to show besides my stupid loans. I’ve been putting away a portion of my income in a matched 401k for the past 10 years but lot of good that did me, it’s lost far more money than it’s ever gained, and it’s expected to give me a mind blowing $15 a month when I retire if I continue at the current rate. My retirement plan is suicide, but more and more I don’t see why I’d wait for retirement age. I have no time or money for hobbies and there’s nothing in my life that brings me joy besides my cats. I think once they’re gone I’ll go with them.

How did your 401k lose more than gained. That would basically be fraud. Just doesn’t work that way. And you left out that you are technically disabled (adhd). I’m not saying shit ain’t fucked up, but this story seems an exaggeration.

How did it lose more than it gained? The loss in interest in investment plus the yearly management fee from the company my employer chose to manage the stupid thing is more than the gains during the good years? I’m no investment expert, all I know is that anytime it gains money it then loses all that shortly after. I’d be better off putting the money in a savings account except at least this way I get employer match. And sure I have ADHD, but it’s not like I’m disabled and unable to work, I’m still working and going to school. You want to tell me that I shouldn’t be able to support myself working over 40 hours a week (and I am not working a minimum wage or “low skilled” job)

If they’ll let you take it and put it in your own 401k I’d suggest doing that. Choose a low-fee brokerage that doesn’t fuck with your investments to incur fees. That’s how they make their money, by taking yours. Choose index funds and let it ride, keep adding when you can, don’t mess with it.

If losses and fees over 10 years came out negative, that is an extremely high indicator of fraud. There are a few exceptions. 1, if you hand picked the investments. 2 if the investments are restricted to like only the company you are working for, which I think has another name instead of 401k.

In the last 10 years the general market is up over 200%.

As for adhd. The point was you are technically not the average person. For us adhders college specifically is often extremely hard. Grades in general before college are rough too, which in turn reduces options for colleges. So it puts us at a solid disadvantage over the average. It certainly is a range, similar to how autism is a spectrum. And adhd can cause some sysmptoms most commonly associated with autism. Some people with adhd can’t work. Those that can often get paid less than thier peers.

In another comment you mentioned that ICE gets a hiring bonus of more than your annual salary. The bonus was $50k I believe. These days for someone in their 30s, that is pretty low for a lot of places except those with a low cost of living.

All in all, you should keep an eye out for that one coworker who seems to know all the details of the 401k and other benefits. Get to know them, and ask questions. They usually love to talk on the subject and can probably help you understand how it all works better. I suspect thier are things you don’t know about that make the situation better than it seems.

Im also curious because over the past 10 years there have been several periods with really high returns.

I don’t know about the other stuff, but I had a job from late 2021 to early-mid 2023. By the time I left the job, the net contributions over about 18 months were $9,992.78, and the balance was $10,340.83.

From the 2nd through the 11th month, the balance was literally less than net contributions.

18 months is very short for a 401k. They usually say to start looking to move the money out of the volatile market and in to stable investments 5 to 10 years before you need it so that you can avoid short term down markets and maybe catch some high spikes.

You said:

So I said, with additional detail:

I’m with the other commenters, baffled about your 401k comments. I changed jobs in 2017 so the 401k I had with that company is a good case study. It’s doubled its balance without a single contribution (obviously, since I left that company).